Do you suffer from FOMI (fear of missing income)?

With interest on cash so high and markets looking volatile, some investors may be tempted to put their spare money in a standard savings account. However, doing so could come with a severe long-term opportunity cost.

When NS&I offered a one-year savings bond paying 6.2% back in August, take-up was swift. By the time it was withdrawn from sale just over a month later, 225,000 customers had committed their savings to it1.

This was unsurprising: 6.2% was the highest rate ever offered on an NS&I bond2 and it came with “HM Treasury’s 100% guarantee on all money invested”3.

Who wouldn’t want to hold one of these products?

As an asset manager that offers equity and bond funds, NS&I and other savings accounts certainly provide healthy competition for our clients’ capital. However, we would still argue that investors who shelter in cash risk missing out on both income and long-term growth.

Fear of missing income in the corporate bond market

Let’s start with bonds. It is currently possible to find high-quality, investment-grade corporate bonds with yields comparable to those offered by NS&I4.

Attractive all-in yield

Admittedly, these bonds carry a higher risk of default than the UK government, which acts as the guarantor of NS&I. And their prices are volatile. This means investors could lose money if conditions move against them (should inflation begin to rise again, for example) and they sell the bonds before they reach maturity.

But these bonds also have a number of clear advantages over the NS&I products. With the latter, you have to commit your money for a full year. That is great… providing that interest rates continue to rise. If they do, at the end of the year, you can simply take your money and put it in another NS&I product or cash account paying an even higher rate of interest.

But here’s the catch. And it’s a big one. Central banks only push interest rates up when they need to bring inflation under control. And, today, inflation is falling rather than rising: CPI in the UK dropped from 6.7% in September to 4.6% in October5 and from 3.7% to 3.2%6 in the US.

If inflation continues to fall, central banks could even cut interest rates. In recent weeks, investors have started to predict the Bank of England will do exactly this in the first half of 20247. This would give investors in corporate bonds three clear advantages over anyone whose cash is tied up in an NS&I savings bond.

- Falling interest rates would drive bond yields down, pushing their prices higher. Holders of NS&I’s savings bond, however, will miss out on these (potential) capital gains.

- Anyone sheltering in cash today will need to find a new home for their savings when their NS&I savings bond matures. A newer version of the same product or another cash savings account will likely pay a much lower rate of interest than today.

- Anyone looking to reinvest the proceeds of their NS&I savings bond may have lost the opportunity to secure the attractive yields on offer in the corporate bond market (remember that these bonds won’t mature for several years, meaning investors have an opportunity to lock in today’s elevated yields for several years longer than NS&I can offer).

Fear of missing dividends and capital gains in the UK stockmarket

Today, the FTSE-All Share index pays out a dividend yield of almost 4%8; the distribution yield on the Artemis Income Fund is slightly higher9. Both figures may be lower than the NS&I savings bond, but remember that dividend payments can continue to grow indefinitely along with corporate profits (particularly if share buybacks continue at their rapid pace).

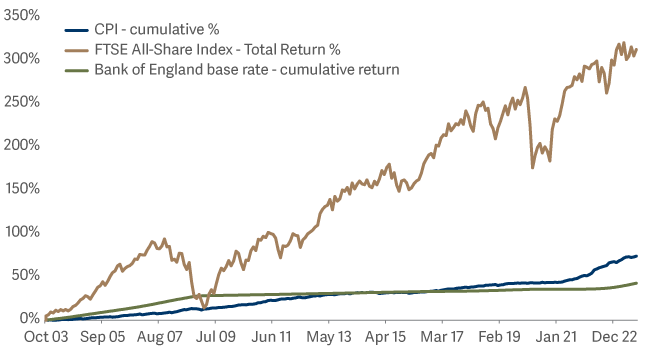

Moreover, equities have historically delivered the highest returns for investors over the long term: the FTSE All-Share index has delivered average annualised returns of 7.8% over the past 20 years and the S&P 500 in the US 11.2%10. Given that UK companies are trading on relatively low multiples of their profits11, there appears to be the potential for significant capital gains if sentiment towards the domestic market improves.

So why can’t investors just take the 6.2% return from an NS&I bond over the next year, then invest the proceeds in an equity fund and enjoy annualised returns of between 7.8% and 11.2% from that point forward?

Performance of FTSE All-Share vs CPI and Bank of England base rate: £ total return

The problem is, of course, volatility. Unlike the slow-but-steady returns from cash, returns from equities are extremely uneven. Data from Bloomberg shows that if you missed the best 15 days of returns from the FTSE All-Share over the past 20 years, you would have made a return of 73.8%. Not bad – but it’s less than a quarter the 312.7% return someone would have made had they remained invested throughout.

Will the turning point for the FTSE All-Share materialise before NS&I’s 6.2% bond matures? Sadly, it is impossible to precisely forecast the stockmarket’s best days. But historically, they have coincided with periods when sentiment and valuations start off unusually depressed (as they are today), then start to look a little brighter. When sentiment changes, markets can move quickly.

Our conclusion... Don’t focus on the short-term

Chasing whatever happens to offer the best return today without thinking about what could happen in the future could prove costly. It is undeniable that a guaranteed 6.2% return sounds attractive, but remember that it comes with an opportunity cost.

Whatever asset you choose, it should be one that is suitable for your time horizon, not the one that looks most attractive in the short term – even if it is yielding 6.2%.

2https://nsandi-corporate.com/news-research/news/nsis-one-year-guaranteed-growth-bonds-and-guaranteed-income-bonds-withdrawn

3https://nsandi-corporate.com/news-research/news/nsis-one-year-guaranteed-growth-bonds-and-guaranteed-income-bonds-withdrawn

4Bloomberg as at 31 October 2023

5https://www.bbc.co.uk/news/business-12196322

6https://www.theguardian.com/business/2023/nov/14/us-inflation-fuel-housing-cpi-fed

7https://www.theguardian.com/business/live/2023/dec/13/uk-gdp-economy-growth-stagnation-falls-october-inflation-interest-rates-boe-fed-business-live

8FTSE Russell

9https://expressapi.fundassist.com/v1/api/Files/981b1c03-b8ce-e811-a82d-005056a3b112

10Bloomberg

11Goldman Sachs as at 25 September 2023